DECIDE WITH CONFIDENCE

| Feature | Benefit | Professional | Industrial |

|---|---|---|---|

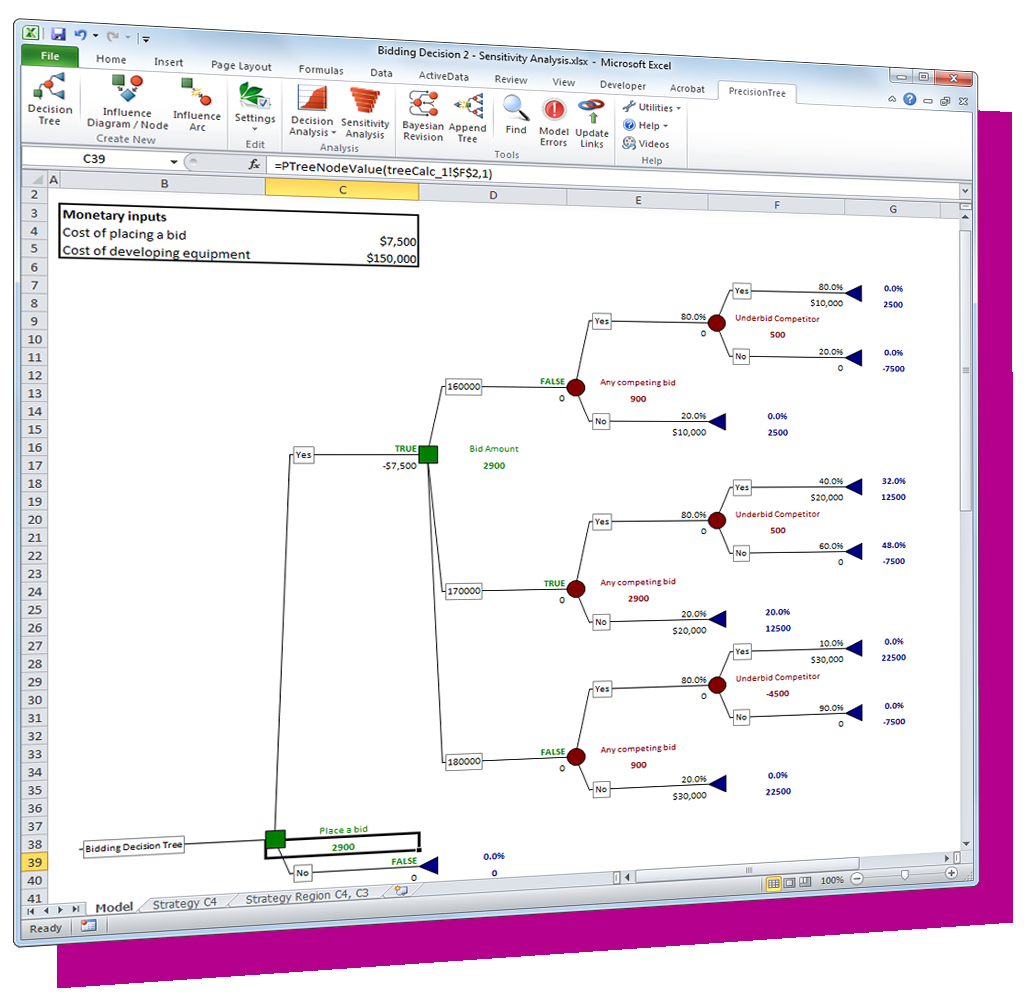

| Decision Trees | Visually understand a decision, identify best options, and communicate results to others |  | |

| Seamless Integration into Microsoft Excel | Never leave your spreadsheet; get up to speed quickly | | |

| Intuitive Toolbars and Right-click Menus | Easy navigation—multiple ways to perform common tasks | | |

| Risk Profile Reports | Shows payoffs and risks of different options | | |

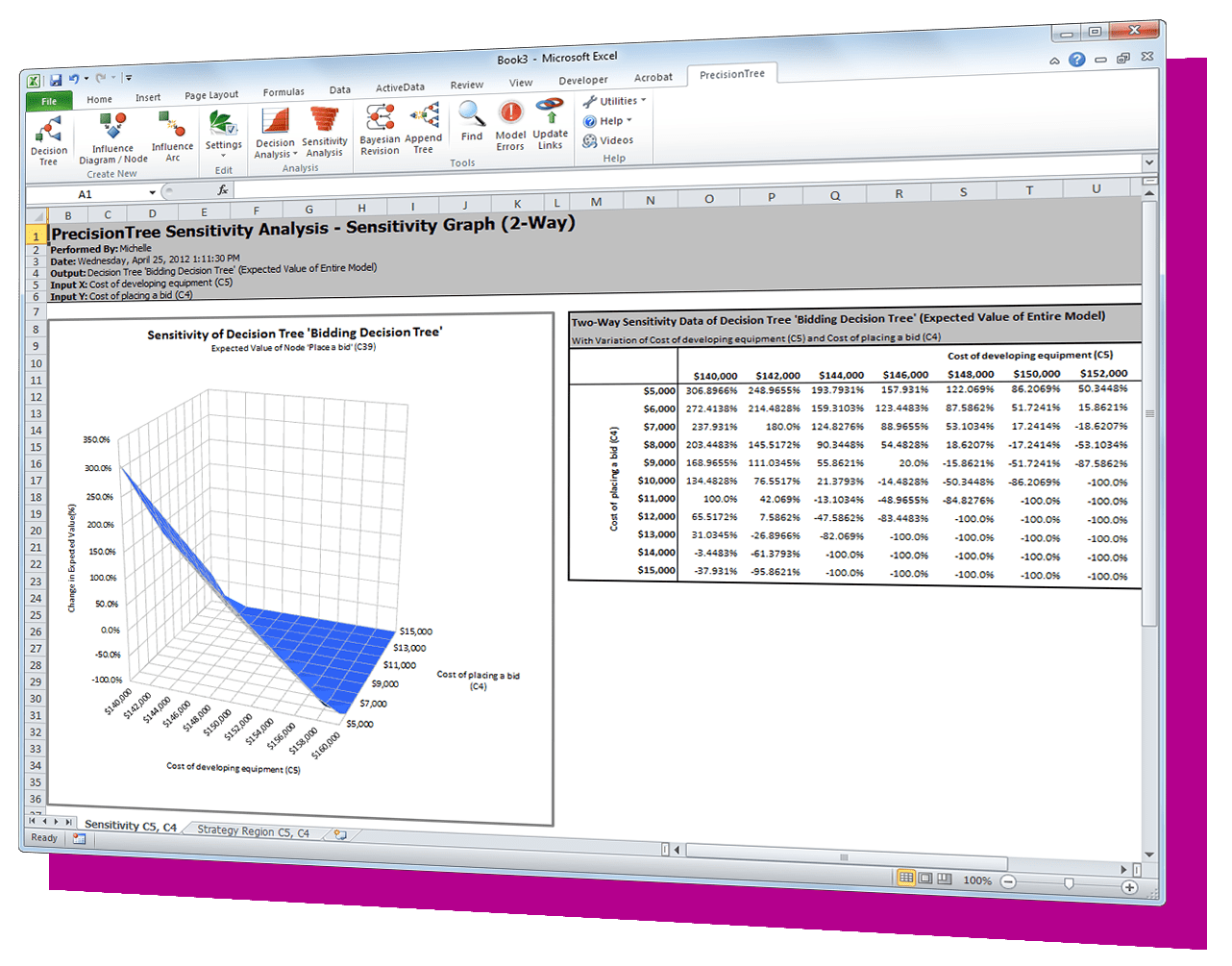

| Sensitivity Analysis | Identifies most influential variables in a decision | | |

| Policy Suggestion Report | Shows optimal decisions and payoffs | | |

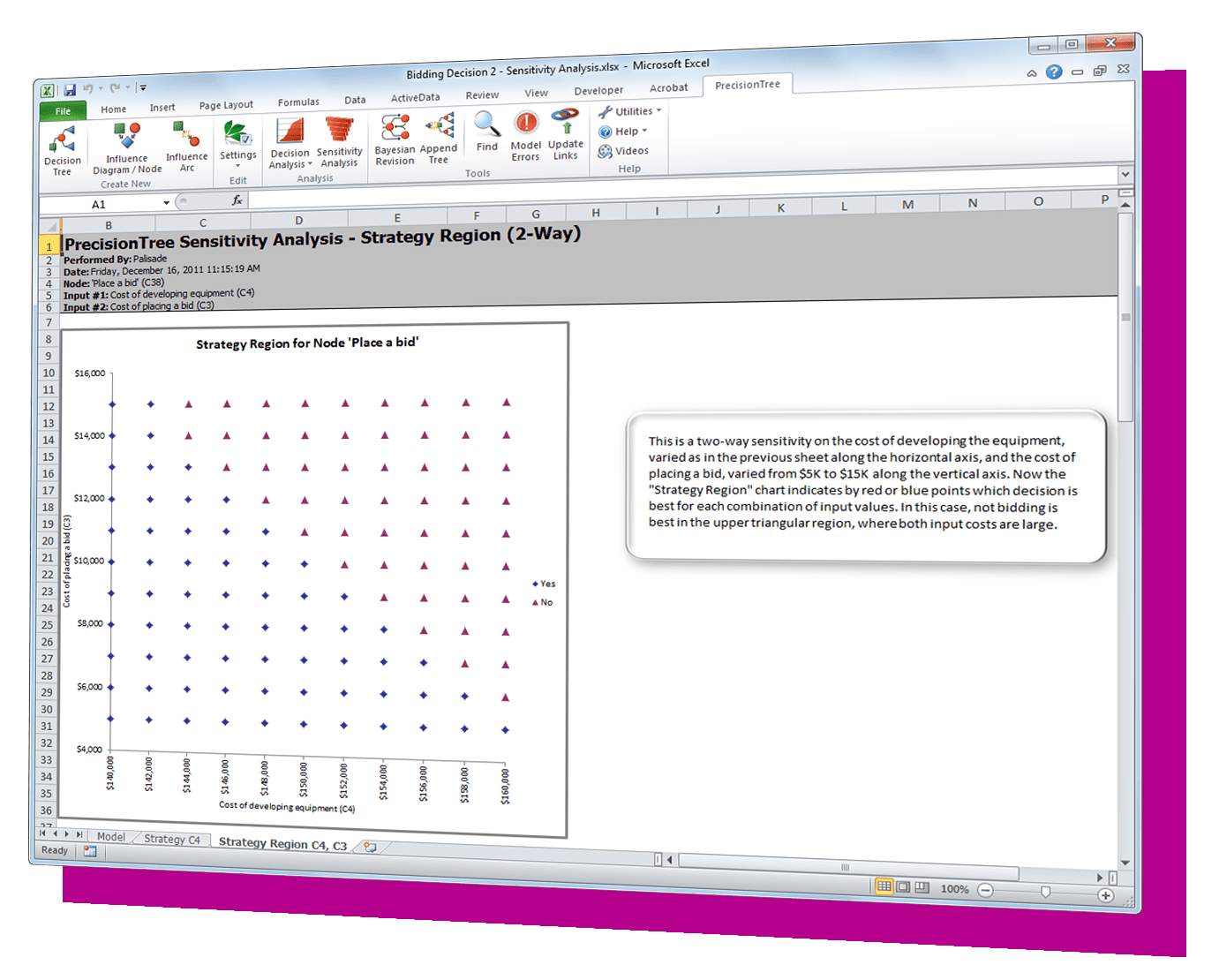

| Strategy Region Graphs | Displays value of decisions over ranges of 1 or 2 variables | | |

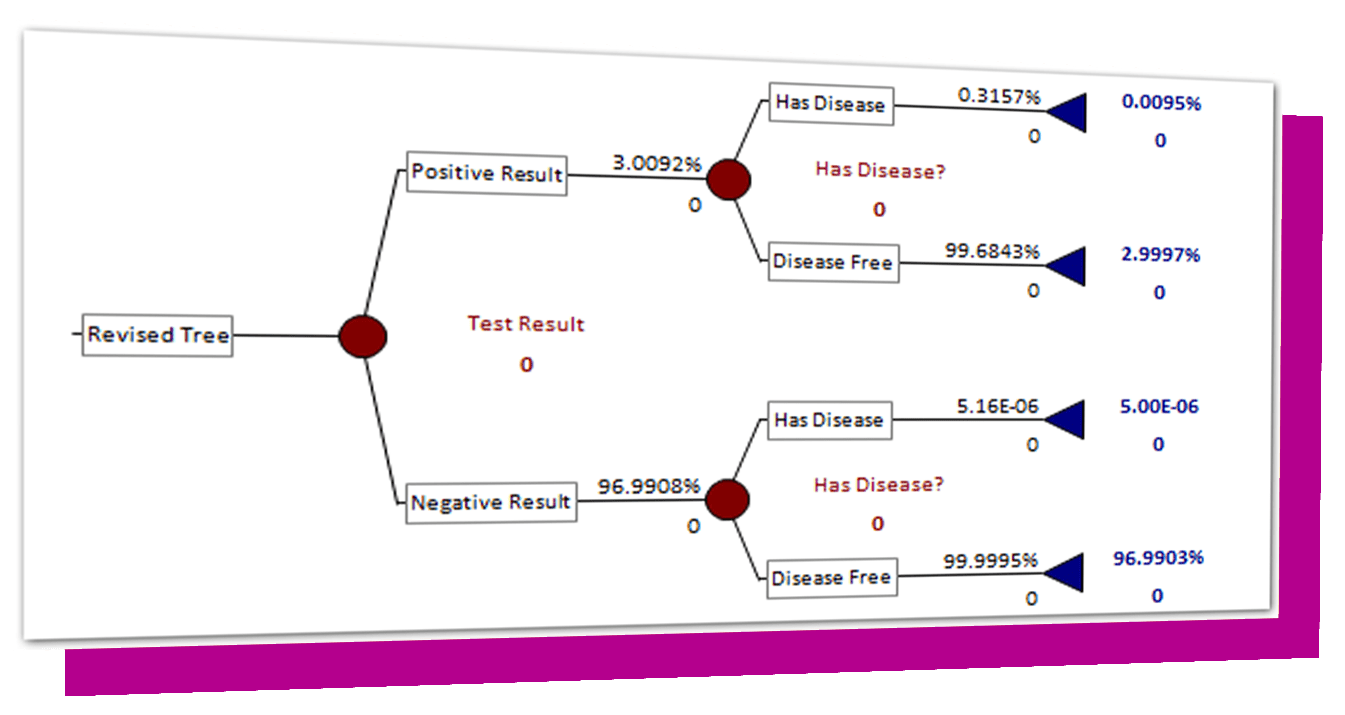

| Bayesian Revision | Reverses chance nodes to show probabilities calculated using Bayes Rule | | |

| Reference nodes and collapsible branches | Streamline large trees for easy navigation | | |

| Logic Nodes | Allows conditional modeling | | |

| Linked Trees and VBA Payoff Calculations | Allows complex payoff computations outside of the tree itself | | |

| Utility Functions | Account for decision maker’s attitude toward risk when calculating the best decision | | |

| PrecisionTree Developer Kit | Automate and customize PrecisionTree with Excel VBA | | |

| Compatibility with @RISK | Account for uncertainty and run Monte Carlo simulations to see all possible outcomes | | |

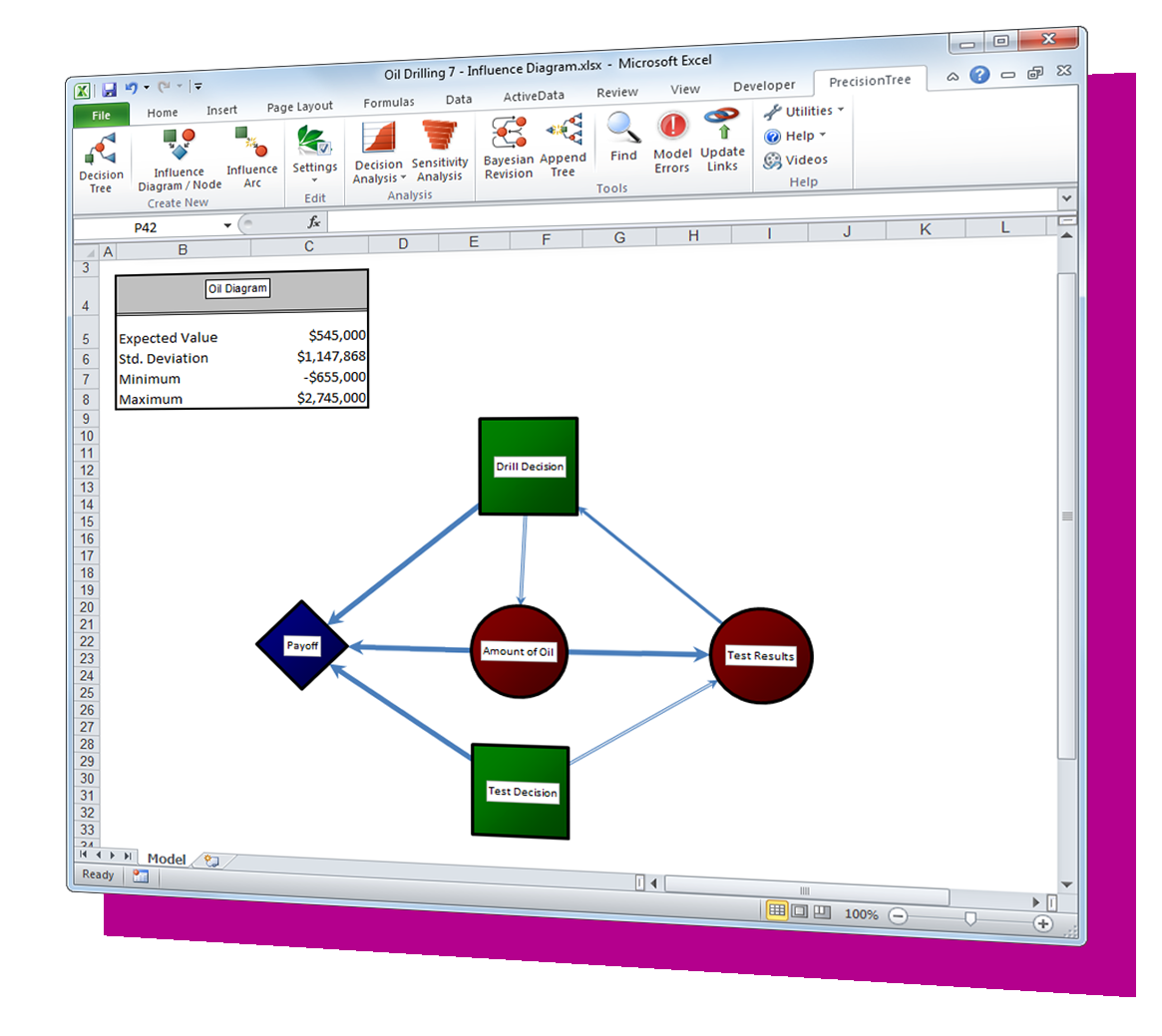

| Influence Diagrams | Visually summarize a decision | | |

| Append Symmetric Subtree | Quickly build large trees, saving a lot of time. | | |

| Insert Node | Easily put a new node inbetween existing nodes in fewer steps. | | |

| Copy Tree Image to Clipboard | Copy and paste any part of a decision tree into Word, PowerPoint, or any application for reports and presentations. | | |

| Number of Tree Nodes | Professional allows up to 1000 nodes per tree; Industrial is unlimited. | |

| Feature | Benefit | Professional | Industrial |

|---|---|---|---|

| Decision Trees | Visually understand a decision, identify best options, and communicate results to others | | |

| Seamless Integration into Microsoft Excel | Never leave your spreadsheet; get up to speed quickly | | |

| Intuitive Toolbars and Right-click Menus | Easy navigation—multiple ways to perform common tasks | | |

| Risk Profile Reports | Shows payoffs and risks of different options | | |

| Sensitivity Analysis | Identifies most influential variables in a decision | | |

| Policy Suggestion Report | Shows optimal decisions and payoffs | | |

| Strategy Region Graphs | Displays value of decisions over ranges of 1 or 2 variables | | |

| Bayesian Revision | Reverses chance nodes to show probabilities calculated using Bayes Rule | | |

| Reference nodes and collapsible branches | Streamline large trees for easy navigation | | |

| Logic Nodes | Allows conditional modeling | | |

| Linked Trees and VBA Payoff Calculations | Allows complex payoff computations outside of the tree itself | | |

| Utility Functions | Account for decision maker’s attitude toward risk when calculating the best decision | | |

| PrecisionTree Developer Kit | Automate and customize PrecisionTree with Excel VBA | | |

| Compatibility with @RISK | Account for uncertainty and run Monte Carlo simulations to see all possible outcomes | | |

| Influence Diagrams | Visually summarize a decision | | |

| Append Symmetric Subtree | Quickly build large trees, saving a lot of time. | | |

| Insert Node | Easily put a new node inbetween existing nodes in fewer steps. | | |

| Copy Tree Image to Clipboard | Copy and paste any part of a decision tree into Word, PowerPoint, or any application for reports and presentations. | | |

| Number of Tree Nodes | Professional allows up to 1000 nodes per tree; Industrial is unlimited. | |

The complete risk and decision analysis toolkit, including @RISK, PrecisionTree, TopRank, NeuralTools, StatTools, Evolver, RISKOptimizer, and ScheduleRiskAnalysis.